The Bankers’ Inheritance

How the boardroom removed a 28-year-old, the regulator broke up his father’s company, and the same three men ended up holding everything that was taken away

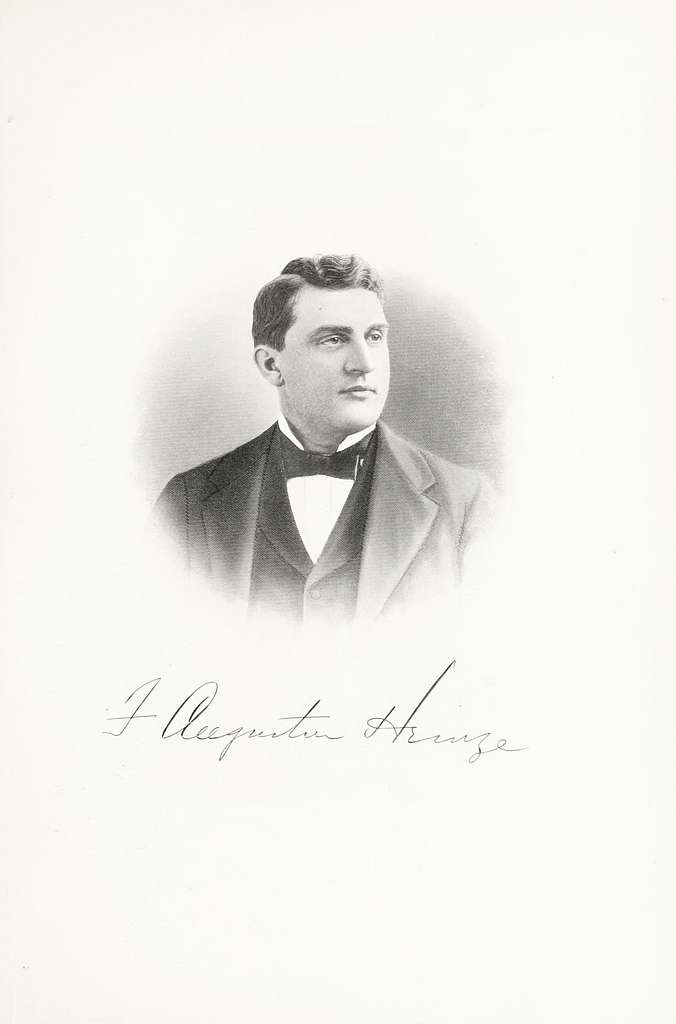

The Son

Henry Baldwin Hyde died on 2 May 1899. He was sixty-five. He had founded the Equitable Life Assurance Society in 1859 with $100,000 in capital and a small office at 98 Broadway, and by the time he died the company held $400 million in assets and 600,000 policyholders. It was the largest life insurance company in America and one of the largest pools of investable capital in the world.

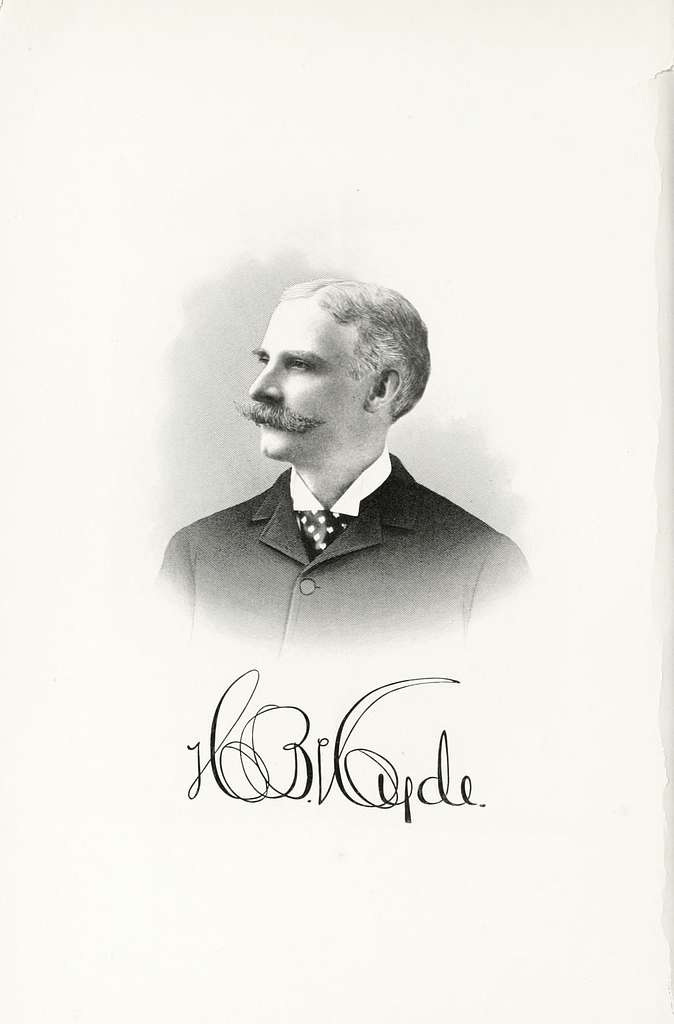

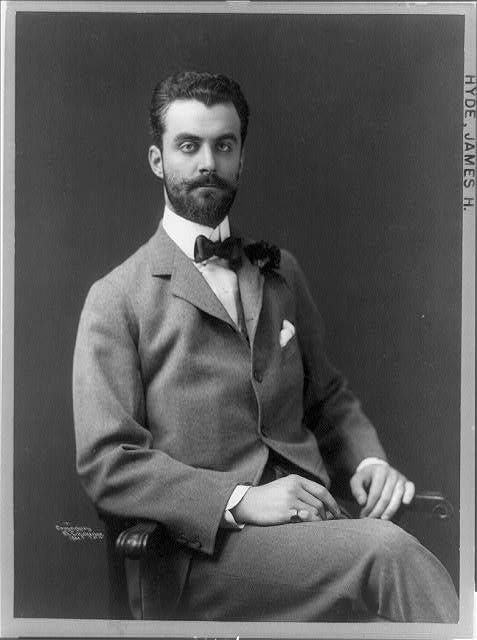

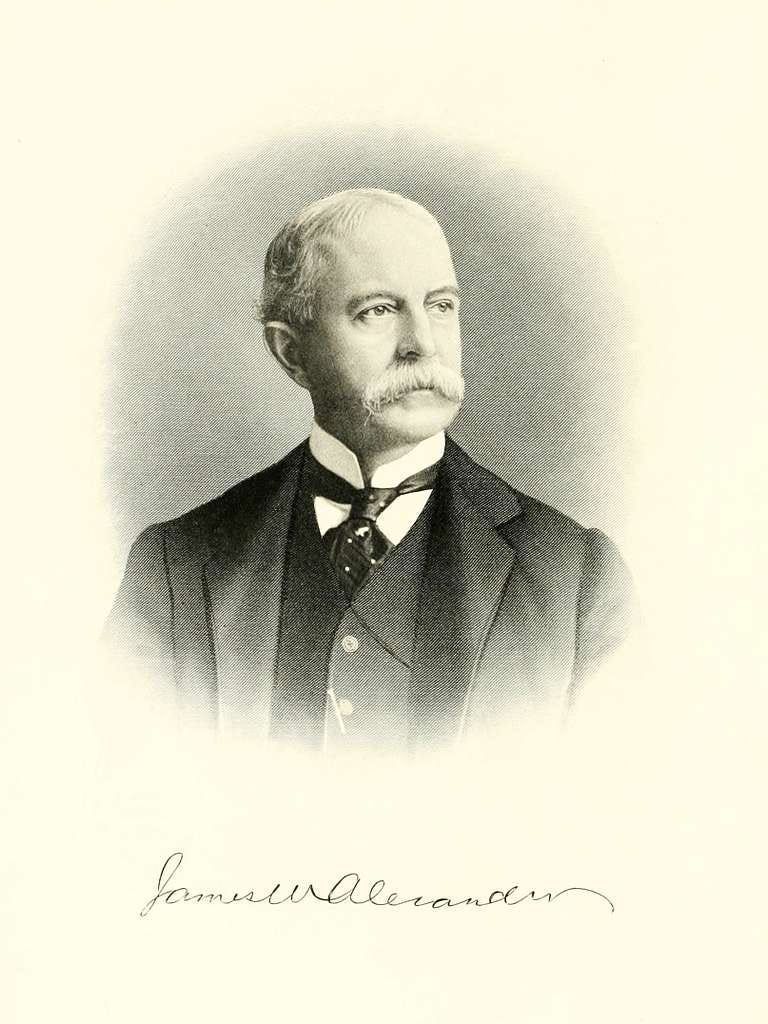

He left his son a controlling 51 per cent stake in the company. James Hazen Hyde was 23 years old. The terms of his father’s will gave him the presidency on his thirtieth birthday in June 1906. In the meantime he took the second vice-presidency. The acting president, James Waddell Alexander, ran the company day to day.

By 1905 the three big New York life insurers — Equitable, Mutual Life, New York Life — together held assets approaching $1.25 billion. Contemporary observers noted the figure exceeded the combined treasuries of “all the great nations of Europe.” (Oxford Global Capitalism History, Gossip, Corporate Reputation, and the 1905 Life Insurance Scandal)

James Hazen Hyde was four-and-a-half months from the chair when his father’s senior officers moved against him.

What life insurance actually was

A life insurance company collects small monthly premiums from hundreds of thousands of policyholders against a future payment on death. The premiums sit in the company’s hands for decades before they pay out. In the meantime they have to be invested somewhere.

By 1905 the American life insurance industry had grown to $2.924 billion in total assets, with 37.7 per cent of it held in securities — stocks and bonds. (Douglass C. North, Life Insurance and Investment Banking at the Time of the Armstrong Investigation, Journal of Economic History, 1954)

That is over a billion dollars of working capital, contributed in tiny instalments by ordinary American families paying for funeral insurance, sitting in the books of three Manhattan companies. The companies could not legally spend it. They could lend it. They could deposit it in banks. They could buy bonds with it. They could underwrite stock issues with it.

The men who ran the three companies sat on the boards of the banks that took their deposits. They sat on the boards of the railroads whose bonds they bought. They sat on the syndicates that floated the new stock. The same men sat on every side of every transaction.

What the boards were doing with the money

The Equitable’s holdings, as the Armstrong Committee would later document, extended across twenty financial institutions. The Equitable owned between 10 and 64 per cent of ten of them.

Equitable Trust Company — book value of stock plus deposits, $17,370,000

National Bank of Commerce — controlled jointly with Mutual Life; the most significant outside shareholding in New York’s second-largest bank

New York Security and Trust Company — held an average $13 million in Equitable deposits, which the trust company then lent on into the call money market

The three big insurance companies between them carried $62,300,000 in cash deposits at New York banks and trusts at year-end 1902 — two to three times what any legitimate operating need would require. The Atlantic reported that actual mid-year deposits “probably ranged from $80 million to $100 million” whenever the firms wanted to make plays in the New York market. (Charles J. Bullock, Life Insurance and Speculation, The Atlantic Monthly, May 1906)

The Equitable’s cash position in November 1903 was $37,029,000. It was dressed down to $24,240,000 for the year-end annual report to the New York Insurance Superintendent. By 31 January 1904 it was back up to $39,677,000. The window was dressed for the regulator and re-opened the moment the regulator looked away. Bullock documented the bookkeeping in The Atlantic Monthly a full eighteen months before the Armstrong Committee began its work.

What Kuhn, Loeb and Morgan were doing on the other side

Kuhn, Loeb & Co. — Jacob Schiff’s firm, the bank closest to E.H. Harriman — sold the Equitable almost $50 million in securities over five and a half years, between 1900 and the start of the Armstrong investigation. Schiff sat on the Equitable board while his firm was the seller. Schiff confirmed this under oath at the Armstrong hearings. (North, 1954)

Standing from left to right: Abraham Zucker, People’s Relief Committee; Isadore Hershfield, who established communication between Jewish families in Europe and America; Rabbi Meyer Berlin, Vice President of the Central Relief Committee; Stanley Bero, Central Relief Committee; Louis Topkis; Morris Engelman, financial secretary of the Central Relief Committee and originator of the plan for American Relief for the Jewish War Sufferers.

New York Life conducted almost all its securities business through a single house, Vermilye and Company: $66 million out of $73 million in purchases over a decade. The company’s vice-president, George W. Perkins, was simultaneously a senior partner at J.P. Morgan & Co. On one Mexican Central Railroad transaction, New York Life put up $1 million at 5 per cent while Morgan’s bank kept $40,000 in profits for arranging the sale of bonds it was selling to a company whose vice-president was a Morgan partner.

The Equitable took $2,500,000 in a $50 million Union Pacific syndicate in 1902-03. It took a loan secured by £2,700,000 in Northern Pacific stock from Harriman in 1901. It took 77,000 shares of Illinois Central as sole security for a $5 million bond. (North, 1954)

Mutual Life held more Pennsylvania Railroad stock than any other shareholder. On one Pennsylvania flotation, Mutual could have purchased $1,666,000 in bonds at par as the largest existing shareholder, and chose instead to buy $4,500,000 through the bank syndicate — paying the underwriting spread back to the bankers who had given it the option to buy direct.

The premiums of American funeral-insurance policyholders were the working capital of the Morgan-Harriman railroad consolidation, the steamship trust, and the steel trust. The insurance executives were taking a fee for handing the money over to the bankers, who were taking a second fee for placing it. The same men were on both sides of the fee.

The money belonged to ordinary American families. The men in the rooms behaved as if it belonged to them.

The ball was the pretext, not the cause

On 31 January 1905 James Hazen Hyde hosted a costume ball at Sherry’s restaurant on Fifth Avenue. Six hundred guests, Versailles theme, the company’s young heir in eighteenth-century French dress. The ball cost roughly $200,000.

A rumour was placed in the New York press that Hyde had charged the cost of the party to the Equitable. The rumour was false. No audit ever found the charge. It did not need to be true to do its work.

The men who placed the rumour were on Hyde’s own board. James Waddell Alexander was the acting president his father had named. E.H. Harriman was the railroad operator whose bonds the Equitable underwrote. Henry Clay Frick was Carnegie’s old partner, by then sitting on the boards that managed the steel and banking industries Morgan had consolidated. Thirty-five officers and agents inside the Equitable signed an internal petition against Hyde. (EBSCO Research Starter: Armstrong Committee Examines the Insurance Industry)

The board’s stated objection was Hyde’s extravagance. The actual objection was that Hyde was four months from inheriting the chair of a company with $400 million in capital, and the senior men around the boardroom did not want him to have it.

Morgan and Harriman both wanted the Equitable’s investment pool under their direct control. The ball gave them an English-language pretext that ran in the newspapers and broke the heir’s reputation before he could take the seat his father had left him.

In June 1905 James Hazen Hyde sold his majority stake to Thomas Fortune Ryan, a Morgan ally, for $2.5 million. He sailed for Paris and stayed there for the next twenty-six years. He died in New York in 1959 having never returned to the insurance industry. He was never charged with any crime. (New York Times obituary, 27 July 1959)

The founder’s son was removed. The pretext was a party.

What the investigation that followed actually did

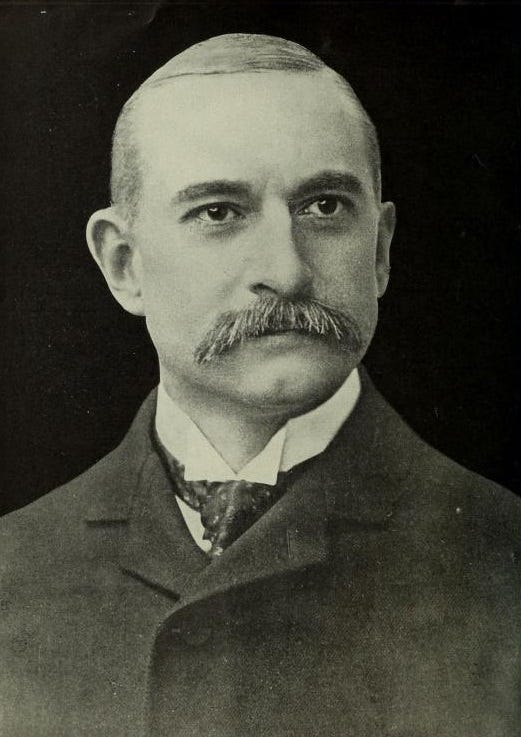

The New York State Legislature, under public pressure from the press coverage of the Hyde affair, established a committee on 1 August 1905. State Senator William W. Armstrong chaired it. The chief counsel was a 43-year-old corporate lawyer named Charles Evans Hughes.

Hughes ran 51 sessions between 6 September and 30 December 1905 and reported on 22 February 1906. The hearings broke open the insurance industry’s relationship with Wall Street. Senator Chauncey Depew of New York admitted under questioning that he had been on a $20,000 annual retainer from the Equitable while serving as a director. Mutual Life had maintained a “house of mirth” in Albany since 1896 for the entertainment of state legislators. Multiple politicians admitted being on insurance company payrolls. (Oxford Global Capitalism History)

The New York Legislature enacted Hughes’s recommendations in eight statutes in April 1906. The two with the largest financial consequence:

First — life insurance companies could no longer own stock, control banks, or underwrite securities. The entire architecture by which the three big insurance companies had been investment banks in everything but name was banned. (Oxford paper, citing the Armstrong Committee Report, NY Legislature, vols. I–X (1906); Yale Law, Statutory Regulation of Life Insurance Investment)

Second — the tontine policy, which had made up two-thirds of all life insurance in force in America in 1905, was prohibited.

The Armstrong Report’s specific finding on stocks: they were “fundamentally objectionable as life insurance investments.” Insurance company stock holdings, which had been around five per cent of total assets, dropped to about two per cent within two years and stayed there for decades. (Yale Law)

A forced sale of roughly $88 million in stock across the industry followed. The price was depressed because every insurance company had to sell at the same time into the same market.

Where the money went

The Armstrong Act required Equitable and Mutual Life to sell their controlling stakes in the National Bank of Commerce — the second-largest bank in New York. The shares had to be sold immediately, in a thin market, to whoever could absorb them.

The buyers were J.P. Morgan & Co., First National Bank, and National City Bank. (EBSCO Armstrong Committee)

The investigation intended to break the Money Trust handed Morgan and his two partner banks the second-largest bank in New York at a forced-sale price.

By 1910 J.P. Morgan had personally acquired the majority of Equitable Life’s capital stock. The Pujo Committee, three years later, recorded that this single shareholding gave Morgan control of resources of $504,000,000 — the institution that had taken his rival Hyde a year to lose. (Pujo Committee Report, 28 February 1913)

The senior men on Henry Baldwin Hyde’s old board, who had moved against the founder’s son in early 1905, watched the regulatory machinery deliver the company to Morgan within five years. The reform broke the insurance industry’s independence. The forced sales transferred control of the industry’s main bank holdings to the three institutions the Pujo Committee would later name as the Money Trust. The founder’s son, in Paris, read about it in the newspapers.

The man who had run the investigation that produced the reform — Charles Evans Hughes — was elected Governor of New York in November 1906, on the strength of his reputation as the man who had broken the insurance industry. He was re-elected in 1908. President Taft appointed him to the Supreme Court in 1910. Harding made him Secretary of State in 1921. Hoover made him Chief Justice of the United States in 1930. (National Governors Association, Charles Evans Hughes; Justia Supreme Court, Chief Justice Hughes)

A career in five offices, built on the investigation that delivered the Equitable to Morgan.

The Clearing House

The reform broke the insurance industry. What it did to the trust companies was worse.

A clearing house is the back office of a banking system. Every day a few hundred New York banks accept cheques drawn on each other. At the end of the day the cheques are netted and the balances are settled. A clearing house is the room where the netting happens.

The New York Clearing House Association was a private cartel of New York commercial banks. It cleared cheques, examined member banks’ books, and in panics it issued clearing-house loan certificates — promissory notes that member banks could use to meet daily settlements in place of cash. The Pujo Committee called the Clearing House “the effective lender of last resort” for the American banking system. There was no Federal Reserve. The Clearing House was as close as anything existed.

Trust companies — institutions like Knickerbocker Trust, Trust Company of America, Lincoln Trust — had originally been Clearing House members. They competed with the national banks for deposits and broker loans. They held lower cash reserves than national banks because they were less regulated. The national banks objected.

In 1903 the Clearing House passed a rule requiring trust company members to maintain cash reserves of 10 to 15 per cent of deposits. The rule took effect on 1 June 1904. Every trust company in New York refused. Every trust company in New York withdrew from the Clearing House rather than meet the reserve requirement. (Ellis W. Tallman and Jon R. Moen, Private Sector Responses to the Panic of 1907, Federal Reserve Bank of Atlanta, March/April 1995, FRASER)

From 1 June 1904 the trust companies could not clear their own cheques through the Clearing House. They had to use a member national bank as a clearing agent. The national bank cleared on the trust’s behalf and charged a fee for the service. The trust company’s solvency on any given day depended on the national bank continuing to extend that service.

The largest trust company in New York that chose to maintain Clearing House access via a member bank was Knickerbocker Trust. Its clearing agent was the National Bank of Commerce — the same bank Morgan had bought out of the Equitable’s forced sale.

Knickerbocker’s president Charles T. Barney sat on the board of the National Bank of Commerce.

J.P. Morgan also sat on the board of the National Bank of Commerce. (Caitlin Frydman and Ellis Tallman, JP Morgan, Trust Companies, and the Impact of the Financial Crisis, NBER 2012)

Two directors of the National Bank of Commerce sat on either side of the clearing relationship that determined whether Knickerbocker Trust would open its doors in the morning. One of them was the president of Knickerbocker. The other was Morgan.

In October 1907, when the run started, the National Bank of Commerce announced it would stop clearing Knickerbocker’s cheques. Knickerbocker fell within twenty-four hours.

What the Syndicate Books say

The Pierpont Morgan Library in New York holds twelve bound ledgers — accession numbers ARC 109 to ARC 117 — that record every securities syndicate Drexel, Morgan & Co. and J.P. Morgan & Co. organised between 1882 and 1933. The bookkeeping is in black ink on heavy ledger paper. They are open to researchers. (Pierpont Morgan Library, J.P. Morgan & Co. Syndicate Books List)

Two researchers — Jon R. Moen of the Federal Reserve Bank of Atlanta and Mary Tone Rodgers of SUNY Oswego — read through the books in the years leading up to 2022 and reconstructed, transaction by transaction, who had been in Morgan’s syndicates between 1901 and 1907.

What they found is in Essays in Economic & Business History, Volume 40, 2022. (Moen & Rodgers, How J.P. Morgan Picked the Winners and Losers in the Panic of 1907)

Every trust company that received emergency liquidity from Morgan during the Panic of 1907 — with one exception, the New York Stock Exchange itself — had previously been a member of a Morgan securities syndicate. The Trust Company of America, which Morgan rescued on 23 October 1907 with $3 million delivered just before closing time, was full of former Morgan syndicate clients.

Knickerbocker Trust was the exception that had to fail. Barney, Knickerbocker’s president, had led one prior syndicate with Morgan — the Pacific Packing & Navigation syndicate of December 1901. It generated a $217,184 loss, the single largest loss on Morgan’s books across two hundred syndicates between 1901 and 1907.

On Sunday 20 October 1907 — the night before the National Bank of Commerce announced it would stop clearing — Barney arrived at Morgan’s house on Madison Avenue to ask for help.

Morgan refused to meet him. (Moen & Rodgers 2022)

The ledger remembered the Pacific Packing loss. The man who ran the firm whose name was on the ledger remembered the man whose syndicate had produced the loss. The decision to let Knickerbocker die was made on a Sunday night in a private library by a man consulting a book.

What the Hepburn Act did to the collateral

The other thing that changed in 1906 was railroad regulation. Congress passed the Hepburn Act on 29 June 1906. The Interstate Commerce Commission was given the power to set maximum railroad rates and to inspect railroad financial records. (National Archives, Hepburn Rate Bill)

Railroad bonds were the single largest asset class on the books of every American insurance company, trust company, and savings bank. Their value depended on the railroads’ ability to set their own freight rates. The Hepburn Act capped the rates. The bonds were repriced downward across the entire American financial system, in the same year the insurance industry was forced to liquidate its bank holdings.

Morgan’s own railroad bond underwriting volume tells the story:

Year Morgan-led railroad bond syndicates 1905 $178,770,000 1906 $92,100,000 1907 $32,476,000

A drop of 82 per cent over two years. (Moen & Rodgers 2022)

The Hepburn rate cap suppressed new bond issuance because the existing bonds were worth less and the new issues commanded lower prices. Trust companies, which had been the largest holders of railroad bonds, were sitting on a depreciating asset base. The Armstrong Act had cut off the insurance companies as a source of demand for new railroad bonds. The Clearing House had cut the trust companies off from emergency liquidity.

By October 1907 the trust company sector was structurally fragile. The system needed a buffer that no longer existed.

What the failed copper corner actually was

The crisis trigger arrived as a stock-corner attempt on a Montana copper company. The version that has come down through the textbooks describes it as a freak event. The contemporary record describes something else.

F. Augustus Heinze was a Montana copper operator who had fought Standard Oil’s Amalgamated Copper Company for fifteen years over underground ore rights in Butte. Standard Oil paid him $12 million in 1906 to settle and sell out his Montana interests. (Federal Reserve Bank of Minneapolis, F. Augustus Heinze of Montana and the Panic of 1907, 1989)

Heinze took the money to New York and bought himself a bank — the Mercantile National Bank — and directorships in five trust companies, ten state banks, six national banks, and four insurance companies. He had become, by late 1906, one of the most heavily over-extended directors in the New York financial system.

His brother Otto Heinze ran a stock brokerage. The brothers had retained United Copper Company, a New Jersey holding company they had incorporated in 1902 with $80 million in authorised capital — a vehicle whose principal remaining value, after the Standard Oil settlement had stripped out the Montana mines, was the float of its own stock.

In October 1907 Otto Heinze attempted to corner that float. The brothers believed short sellers had borrowed United Copper shares to sell, and that the family controlled enough stock to squeeze them. On 14 October the shares ran from $39 to $60 in fifteen minutes on the Curb Market.

The corner failed within forty-eight hours. The short sellers found stock from other sources. United Copper collapsed.

The Standard Oil group — which had paid Heinze $12 million the previous year to get him out of Montana, and which controlled Amalgamated Copper — placed reports in the financial press accelerating United Copper’s fall. (New England Historical Society, The Panic of 1907 and the Maine Man Who Caused It)

The Heinze brothers’ financial position collapsed with the stock. Within forty-eight hours, every bank Heinze sat on the board of faced a deposit run. The Clearing House announced it would aid the Morse-affiliated national banks only on condition that Morse retire completely from banking in New York. Heinze was forced to resign from Mercantile National Bank.

The shock travelled along the directorship chain. Charles T. Barney of Knickerbocker had business associations with Morse. The National Bank of Commerce, on which Morgan sat, announced it would no longer clear for Knickerbocker.

The panic that broke the American banking system began as a fight between Standard Oil and a Montana copper man Standard Oil had already paid to leave Montana. The men whose interests were threatened by the chaos that followed were the same men whose institutions absorbed the wreckage.

The Money Pool

On the afternoon of 24 October 1907 the call money rate on the floor of the New York Stock Exchange opened at 6 per cent. By the afternoon it had reached 100 per cent annualised with no money offered at the bid. The brokers could not borrow at any price. (Federal Reserve History, The Panic of 1907; Tallman & Moen, Lessons from the Panic of 1907, 1990)

R.H. Thomas, the president of the Exchange, left the trading floor and walked to Morgan’s office.

Morgan announced the formation of a Money Pool — a private syndicate of bank money that would lend to brokers on the floor that afternoon at 10 per cent. The pool was approximately $10 million from the Morgan group, $2 million from First National Bank, $500,000 from Kuhn Loeb, and other contributions. The floor brokers borrowed $18.95 million from the pool by close of business. (Tallman & Moen 1990)

The previous evening, Wednesday 23 October, Morgan had met with Treasury Secretary George Cortelyou in New York. The following morning Cortelyou deposited $25 million of US Treasury funds in New York national banks. By 31 October, total Treasury deposits in New York reached $37.6 million, with another $36 million in small bills shipped in to meet over-the-counter cash runs. By mid-November the US Treasury’s entire working capital had been drawn down to $5 million. (Tallman & Moen 1990)

The US federal government emptied its operating account into the New York banking system at Morgan’s request. Morgan decided which banks the federal money went to. Cortelyou took the call.

John D. Rockefeller deposited $10 million at Union Trust and publicly announced he was backing Morgan. The signal was understood. (Gotham Center for NYC History, The Panic of 1907: How JP Morgan Took Over Wall Street)

The Clearing House issued $101 million in clearing-house loan certificates to its member banks in New York between 26 October and 26 December 1907. No certificates were issued to trust companies. By 19 December, New York trust company deposits had fallen 36 per cent. New York national bank deposits had risen.

The panic transferred deposits from trust companies, which were not members of the Clearing House, to the national banks that were. The Clearing House members were the institutions Morgan, Baker, and Stillman controlled.

The Money Trust, named

The Pujo Committee — the House Banking and Currency subcommittee that investigated American financial concentration between 1912 and 1913 — defined the inner group of the Money Trust in formal language:

“J. P. Morgan & Co., the recognized leaders, and George F. Baker and James Stillman in their individual capacities and in their joint administration and control of the First National Bank, the National City Bank, the National Bank of Commerce, the Chase National Bank, the Guaranty Trust Co., and the Bankers Trust Co.”

Combined known resources in those institutions alone: in excess of $1,300,000,000. Adding Morgan’s controlling stake in Equitable Life: $2,104,000,000. (Pujo Committee Report, 28 February 1913)

George F. Baker of First National Bank held 46 directorships in 37 of the largest American corporations. He was the oldest trustee of Mutual Life Insurance. His railroads carried 80 per cent of the anthracite coal mined in Pennsylvania.

James Stillman of National City Bank held 47,498 shares of the bank’s 250,000 in his own name. National City’s reach, with its securities affiliate National City Company, was approximately $600 million in banking resources. Stillman and William Rockefeller had organised Amalgamated Copper — the same Amalgamated whose conflict with the Heinze brothers had detonated the 1907 panic.

The three men, between them, held 341 directorships across 112 corporations with aggregate resources of $22.245 billion. Morgan & Co. alone held 72 directorships across 47 of the greatest corporations.

George F. Baker testified before the Pujo Committee. Asked whether the concentration of financial power he and his colleagues had assembled was healthy for the country, he gave one answer:

“I think it has gone about far enough. If it got into bad hands, it would be very bad.”

He said it in his own voice in 1913, three years before he died, after a working life spent at the centre of the network the Pujo Committee was investigating. The man who had built the Money Trust was telling Congress on the record that the structure he had built was dangerous in the wrong hands.

He did not propose to dismantle it. He proposed to keep it in his own.

Tennessee Coal, Iron & Railroad

On Sunday 3 November 1907 a brokerage house called Moore and Schley told Morgan it could not meet its Monday morning obligations. The firm had borrowed $25 million from New York banks using a large block of stock in the Tennessee Coal, Iron & Railroad Company as collateral. TCI was the largest steel producer in the American South. It owned more coal and iron ore than any American firm except U.S. Steel. It produced fifty-nine per cent of US open-hearth steel rails. Edward Harriman had ordered 160,000 tons of TCI rails for his railroad earlier that year. TCI was planning to double its capacity.

Morgan instructed U.S. Steel to buy TCI. U.S. Steel’s own finance committee recommended against the purchase. Morgan overruled the committee.

Antitrust approval was needed. On Monday 4 November 1907, Elbert Gary (chairman of U.S. Steel) and Henry Clay Frick (the same Frick who had been on the Equitable board moving against Hyde in 1905) travelled to the White House and met President Theodore Roosevelt before the New York Stock Exchange opened.

Roosevelt wrote to Attorney General Charles Bonaparte the same day. The letter was transmitted to the Senate on 6 January 1909 and is in the government record:

“They state that there is a certain business firm (the name of which I have not been told, but which is of real importance in New York business circles) which will undoubtedly fail this week if help is not given. Among its assets are a majority of the securities of the Tennessee Coal Company.”

“I answered that while of course I could not advise them to take the action proposed, I felt it no public duty of mine to interpose any objection.”

The deal closed that day. U.S. Steel paid for TCI in U.S. Steel five per cent gold bonds — not cash, paper.

Morgan took the South’s largest steel producer, in a forced sale, with paper, the morning his partners walked out of the White House with the President’s commitment not to interpose. The price has never been definitively established as a number against true value. The U.S. Bureau of Corporations had estimated U.S. Steel’s overall 1901 capitalisation was inflated by $700 million in “water” against true value of $682 million. The TCI purchase price, in the assessment of contemporary observers, was far below what the assets were worth.

President Taft’s Justice Department filed suit against U.S. Steel in November 1911 alleging the TCI acquisition had been an unlawful expansion of monopoly. The case ran for nine years. The Supreme Court decided it 4-3 on 1 March 1920 in United States v. United States Steel Corporation, 251 U.S. 417, holding that U.S. Steel was not a monopoly because its market share by 1911 was only 40 per cent. The Court explicitly weighed Roosevelt’s 1907 approval of the TCI deal in U.S. Steel’s favour. (U.S. v. U.S. Steel Corp., 251 U.S. 417 (1920))

The President’s verbal approval, given in a Monday morning meeting before the markets opened, became the legal precedent that protected the acquisition twelve years later in the Supreme Court.

What had moved

In the seven years between James Hazen Hyde’s father dying and the TCI deal closing, the following had moved.

The Equitable, the largest life insurance company in America, had been taken from its founder’s son and absorbed by Morgan. The other two large insurance companies, Mutual and New York Life, had been forced by the Armstrong reforms to sell their controlling stakes in the National Bank of Commerce, which Morgan and his two partner banks then bought. The trust companies had been excluded from the Clearing House and were now operating without an emergency liquidity backstop. Railroad bond values had been suppressed by the Hepburn rate cap, weakening trust company balance sheets. A failed copper corner — between a man Standard Oil had paid to leave Montana and the Standard Oil interests that had paid him — had triggered a run that the absent backstop could not absorb. Morgan had stepped in as the only available substitute, in concert with Stillman, Baker, the US Treasury, and Rockefeller. Knickerbocker Trust had been allowed to die because its president was the wrong syndicate partner. Trust Company of America had been saved because its board was the right one. U.S. Steel had absorbed the largest steel competitor in the South in a forced sale, paid for in paper, with the President’s verbal blessing. Charles Evans Hughes had become Governor of New York on the strength of the investigation that delivered the Equitable to Morgan.

By the end of 1907 the same three institutions — J.P. Morgan & Co., First National Bank, National City Bank — held 341 directorships across 112 corporations with $22.245 billion in resources. The man who had run the insurance investigation was Governor. The man who had led the reform of the railroad rates was President and had given verbal approval to the largest forced acquisition of the panic.

The system that emerged from the 1907 panic was the system three men had built. The reforms that had been intended to limit it had concentrated it. The crisis that had been intended to break it had been the moment it consolidated.

Six years later the same men were on the train to Jekyll Island, drafting the central bank they would use to finance the war.

The bank they built was not new. It was the same syndicate, with a federal charter.

What documents establish

Henry Baldwin Hyde founded the Equitable Life Assurance Society on 26 July 1859. He died on 2 May 1899. His son James Hazen Hyde inherited 51 per cent of the company at age 23. (American Antiquarian Society memorial)

The January 1905 costume ball at Sherry’s was the public pretext for the boardroom removal of Hyde. The rumour that Hyde had charged the ball to Equitable was false and never substantiated by audit. (Oxford Global Capitalism History)

The Armstrong Committee’s 1906 statutes banned life insurance companies from owning stock, controlling banks, or underwriting securities. (Yale Law)

The forced sale of National Bank of Commerce shares went to Morgan, First National, and National City. By 1910 Morgan personally controlled the Equitable. (Pujo Committee, 1913)

The New York Clearing House excluded trust companies in June 1904. Knickerbocker Trust cleared through the National Bank of Commerce, on whose board both its president and J.P. Morgan sat. (Tallman & Moen, FRASER 1995; Frydman & Hilt, NBER 2012)

The Hepburn Act of 29 June 1906 capped railroad rates and depressed railroad bond values, contracting the asset base of trust companies and insurance funds. (National Archives)

The Pierpont Morgan Library Syndicate Books (ARC 109–117) record every Morgan securities syndicate from 1882 to 1933. Moen & Rodgers (2022) demonstrate that emergency liquidity in 1907 was extended only to prior Morgan syndicate partners, with Knickerbocker the documented exception. (Pierpont Morgan Library; Moen & Rodgers 2022)

Treasury Secretary George Cortelyou deposited $25 million in Morgan-affiliated banks on 24 October 1907 at Morgan’s request, drawing down US federal working capital to $5 million by mid-November. (Tallman & Moen, FRASER 1990)

Roosevelt’s 4 November 1907 letter to Attorney General Bonaparte recorded his approval of U.S. Steel’s TCI acquisition; the Supreme Court relied on this in U.S. v. U.S. Steel, 251 U.S. 417 (1920). (Roosevelt to Bonaparte, US Serial Set; Supreme Court ruling)

Compiled from the Pujo Committee Report (1913), the Pierpont Morgan Library Syndicate Books (ARC 109-117), the Federal Reserve Bank of Atlanta research papers on FRASER, the National Archives, the US Serial Set, the Library of Congress legal archives, the Journal of Economic History (Cambridge), the Yale Law Journal archive, the Oxford Global Capitalism History case archive, and the New York Times historical record.

Hi Ali. Your skills and research continue to astound me how you unopick these tangled webs of deception and intrusive. There's always Jewish hands at work. Thank you the many hours of work you put in Very interesting and shocking content

Walking through a Kroger store, greatly annoyed at the every 20 minute vaccine plug, between Muzak songs,…. I became curious enough to lookup ‘who owns Kroger’.

Well, wouldn’t you just know it, same controlling interest that has most big corps.

Same smell as six score years back. And that admission as to if that much power fell ‘into the wrong hands’

The staggering trillions (much handled by Blackrock) to bribe every institution, fed, state & local governments (foreign too - Belorus leader went public about the bribery), media , etc. to foist the covid nonsense, displays the complete corruption we are suffering under.

…& war